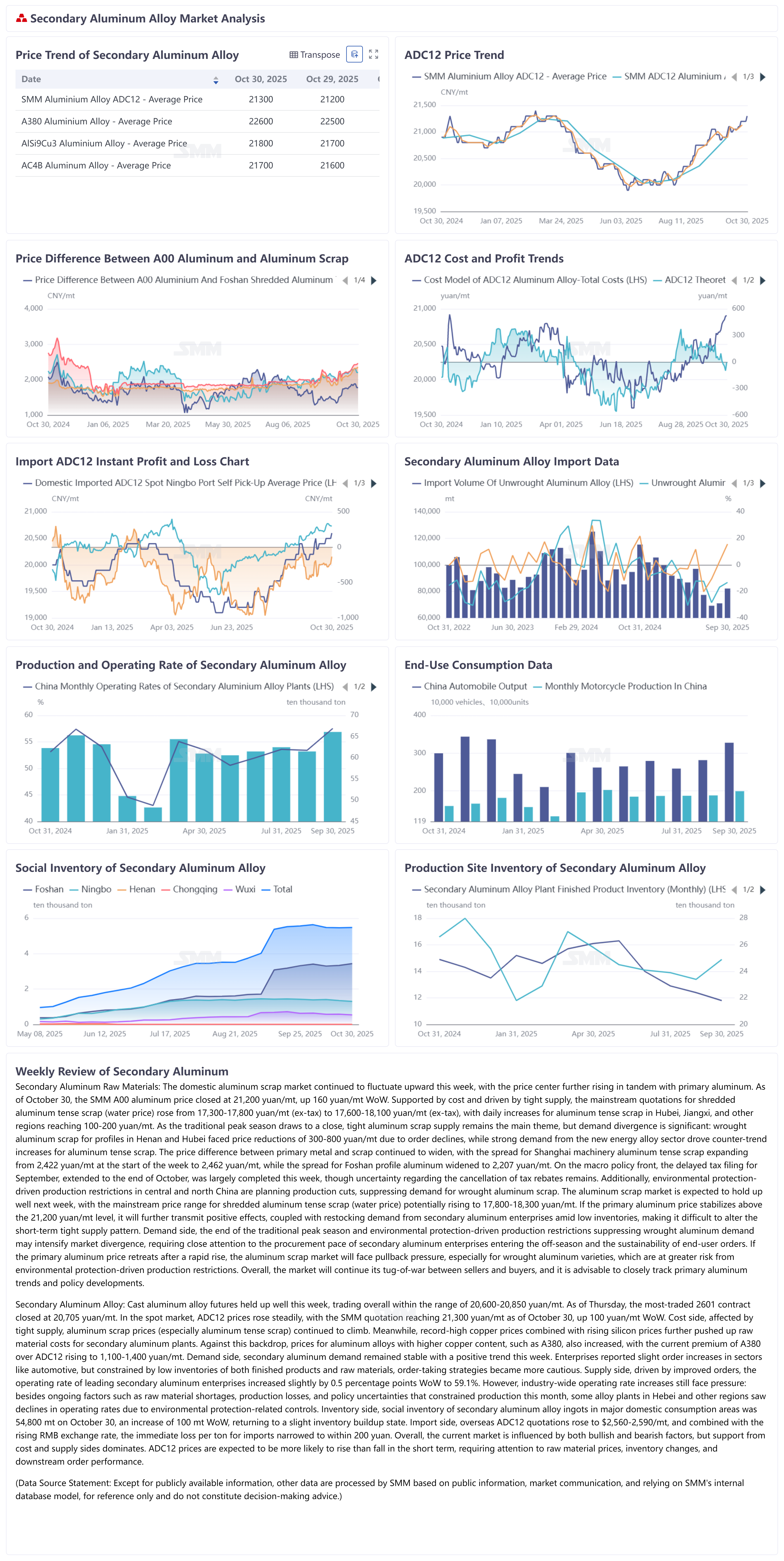

This week, the domestic aluminum scrap market continued to fluctuate upward, with the price center further rising in line with primary aluminum movements. As of October 30, the SMM A00 aluminum price closed at 21,200 yuan/mt, up 160 yuan/mt WoW. Supported by cost factors and tight supply, the mainstream quotations for shredded aluminum tense scrap (water price) rose from 17,300-17,800 yuan/mt (ex-tax) to 17,600-18,100 yuan/mt (ex-tax), with daily increases for aluminum tense scrap in Hubei and Jiangxi reaching 100-200 yuan/mt. As the traditional peak season draws to a close, tight aluminum scrap supply remains the dominant theme, but demand has diverged significantly: processed aluminum scrap for profiles in Henan and Hubei saw prices driven down by 300-800 yuan/mt due to declining orders, while robust demand from the new energy alloy sector pushed up aluminum tense scrap prices against the trend. The price difference between primary metal and scrap continued to widen, with the spread for Shanghai machinery aluminum tense scrap increasing from 2,422 yuan/mt at the beginning of the week to 2,462 yuan/mt, while the price difference for Foshan profile aluminum widened to 2,207 yuan/mt. On the macro policy front, the delayed tax filing for enterprises from September was largely completed this week by the October month-end, though uncertainty around the cancellation of tax rebates persists. Meanwhile, environmental protection-driven production restrictions in central and north China are expected to lead to production cuts, suppressing demand for processed aluminum scrap. Next week, the aluminum scrap market is projected to hold up well, with the mainstream price range for shredded aluminum tense scrap (water price) likely to shift upward to 17,800-18,300 yuan/mt. If the primary aluminum price stabilizes above the 21,200 yuan/mt mark, it will further transmit positive momentum. Coupled with restocking demand from secondary aluminum enterprises amid low inventory, the short-term tight supply situation is unlikely to ease. Demand side, the end of the traditional peak season and environmental protection-related production restrictions suppressing demand for processed aluminum scrap may exacerbate market divergence. Close attention should be paid to the procurement pace of raw materials by secondary aluminum enterprises as they enter the off-season and the sustainability of end-user orders. If the primary aluminum price retreats after a rapid rise, the aluminum scrap market will face pullback pressure, particularly for processed aluminum scrap varieties, which are at higher risk due to environmental protection-driven production restrictions. Overall, the market is expected to continue its tug-of-war between sellers and buyers, and it is advisable to closely monitor primary aluminum trends and policy developments.

This week, cast aluminum alloy futures held up well, trading within the range of 20,600–20,850 yuan/mt. As of Thursday, the most-traded 2601 contract closed at 20,705 yuan/mt. In the spot market, ADC12 prices rose steadily, with the SMM price reaching 21,300 yuan/mt as of October 30, up 100 yuan/mt WoW. Cost side, driven by tight supply, aluminum scrap (especially aluminum tense scrap) prices continued to climb. At the same time, record-high copper prices combined with rising silicon prices further increased raw material costs for secondary aluminum plants. Against this backdrop, prices for aluminum alloys with higher copper content, such as A380, also rose. Currently, the premium of A380 over ADC12 has widened to 1,100–1,400 yuan/mt. Demand side, secondary aluminum demand remained stable with slight improvement this week. Enterprises reported modest order increases from sectors like automotive, but due to low inventories of both finished products and raw materials, order-taking strategies became more cautious. Supply side, supported by improved orders, the operating rate of leading secondary aluminum enterprises rose 0.5 percentage points WoW to 59.1%. However, industry-wide operating rates still faced upward pressure: in addition to persistent challenges such as raw material shortages, production losses, and policy uncertainties, some alloy plants in Hebei and other regions saw lower operating rates due to environmental protection-related controls. Inventory side, social inventory of secondary aluminum alloy ingots in major domestic consumption areas stood at 54,800 mt on October 30, up 100 mt from the previous Thursday, indicating a slight inventory buildup. Import side, overseas ADC12 offers increased to $2,560–2,590/mt, and with the strengthening RMB, the immediate import loss per ton narrowed to below 200 yuan. Overall, bullish and bearish factors are intertwined in the current market, but cost and supply-side support dominate. ADC12 prices are more likely to rise than fall in the short term, with attention needed on raw material prices, inventory changes, and downstream order performance.